2025

Connecting banking apps with ChatGPT to redefine how users choose credit cards.

José Manuel Zevallos, Stanford University

Rol

Product Design

UX Strategy

UI Design

Category

FintechAI IntegrationiOS / Android

Project Type

BankingConversational AIConcept Design

Professional website of José Manuel Zevallos

Digital Media Designer © 2025. All rights reserved.

zevallosj147@gmail.com

LinkedIn: in/jmanuelzevallos

Challenge

Today, users must manually compare multiple banking apps to understand which credit card best fits their needs. Each bank promotes its own products, creating fragmented, biased, and time-consuming experiences. This complexity not only limits transparency but also increases friction in decision-making, leaving users overwhelmed and often choosing suboptimal cards. There is no unified experience that helps users make smart, personalized financial decisions across institutions.

Hypothesis

If banking apps were securely connected through ChatGPT, users could authenticate once and instantly compare their eligibility, benefits, and offers across all their banks. By combining conversational AI with secure login (Face ID + API integrations), users would receive objective recommendations based on preferences, such as cashback, travel, or dining rewards reducing friction, improving trust, and accelerating credit-card adoption.

Summary

This proof of concept explores how ChatGPT can serve as a financial orchestrator, connecting multiple banking apps to redefine how users choose and request credit cards. By unifying authentication and decision-making into a single conversational experience, the flow empowers users with clarity, personalization, and control, while helping banks increase product visibility and digital conversion.

Problem Users Faced

Users struggle to identify which credit card offers the best value without logging into multiple apps, reading complex terms, or comparing unclear benefits. The current process is tedious, opaque, and biased toward each bank’s ecosystem, discouraging users from exploring better options.

Business Objective

To enable a cross-banking, AI-driven experience that increases user engagement and conversion rates for credit-card products, while positioning the bank ecosystem as transparent, data-driven, and customer-centric through open-banking integrations with ChatGPT.

Product Owner & Business Request

The Product Owner requested a conceptual prototype demonstrating how an AI assistant like ChatGPT could integrate securely with multiple banking apps to streamline credit-card discovery and acquisition. The goal is to validate the potential impact on user trust, conversion rate, and perceived innovation through a seamless conversational flow.

Applied Methodology

This project applies a Lean Product Discovery & AI-Driven Design methodology, combining Service Design, Human-Centered Design (HCD), and Experiment-Based Validation to explore how conversational interfaces can transform cross-banking experiences.

Proof of concept (PoC) English

Proof of concept (PoC) Spanish

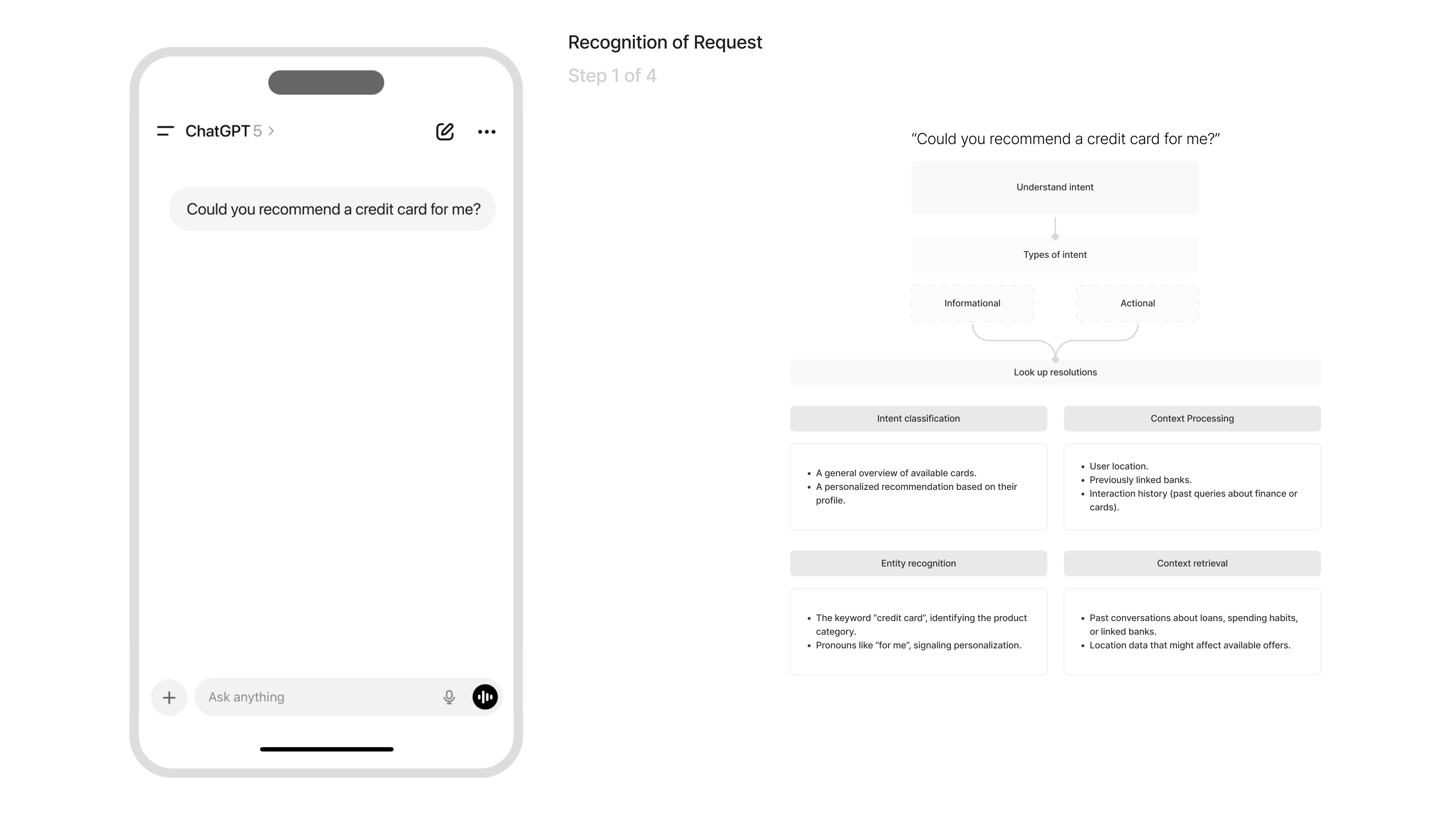

Recognition of Request

Purpose: Understand the user’s intent and classify the type of request.

At this stage, the system interprets the message “Could you recommend a credit card for me?”.ChatGPT identifies the user’s goal (getting a credit card recommendation) and determines whether the request is informational or action-oriented.It then performs a structured lookup across different resolution paths:

- Intent classification: Determines whether the user wants a general list of cards or a personalized recommendation based on their profile.

- Entity recognition: Detects keywords like “credit card” and pronouns like “for me”, which signal personalization.

- Context processing & retrieval: Considers location, linked banks, and interaction history.

This step ensures contextual accuracy, compliance, and personalization before the model proceeds.

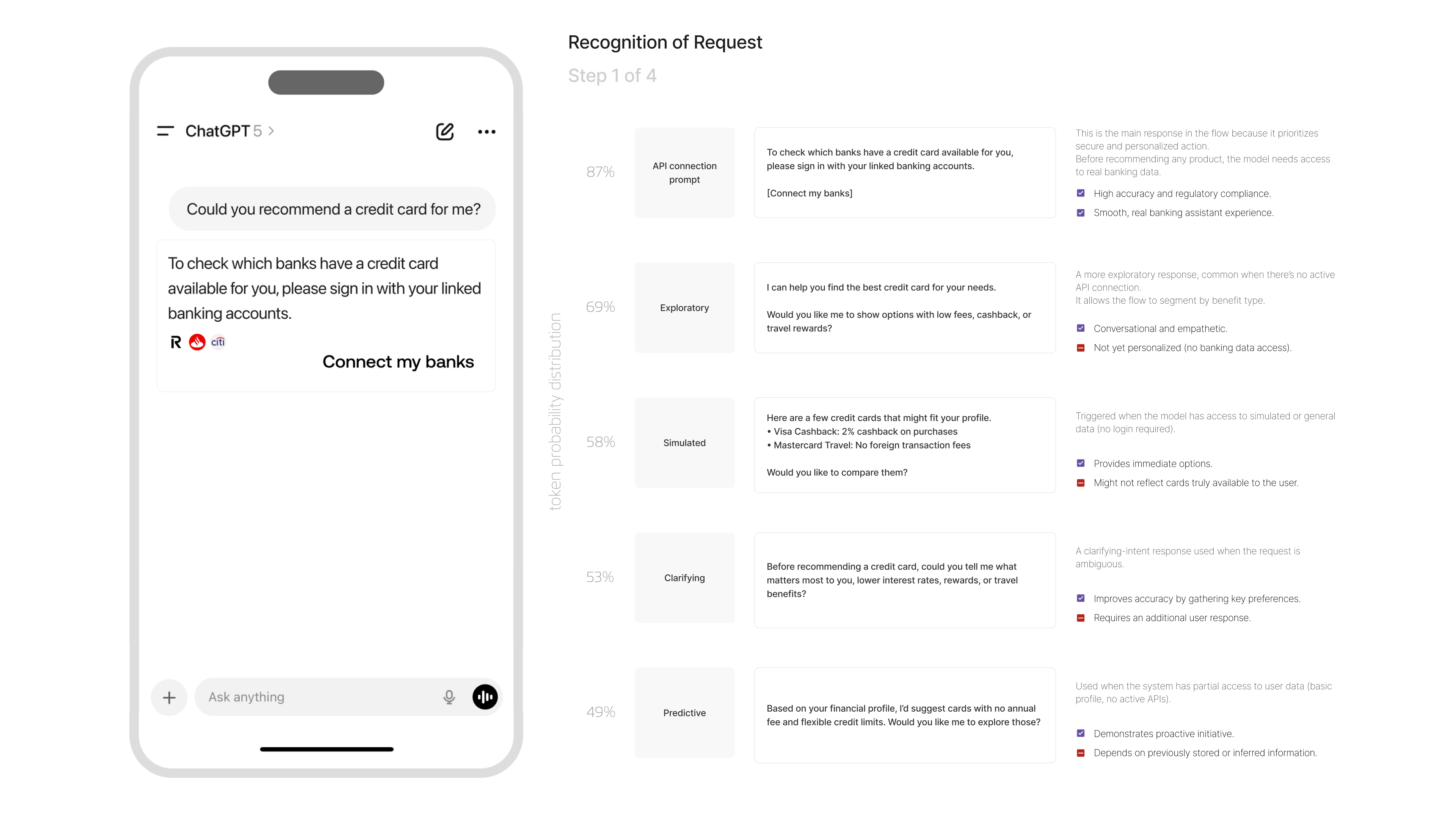

The system evaluates multiple possible response styles based on the user’s request, weighing each option according to regulatory constraints, personalization requirements, and conversational context.

It analyzes whether the best response is a secure API-connection prompt, a more exploratory conversational reply, a simulated example, a clarifying question, or a predictive suggestion.

The model does this by calculating token-level probability distributions for each reasoning path, ultimately selecting the approach that balances compliance, personalization, and user intent. This ensures that before any action is taken, the assistant understands both what the user wants and the safest, most accurate way to proceed.

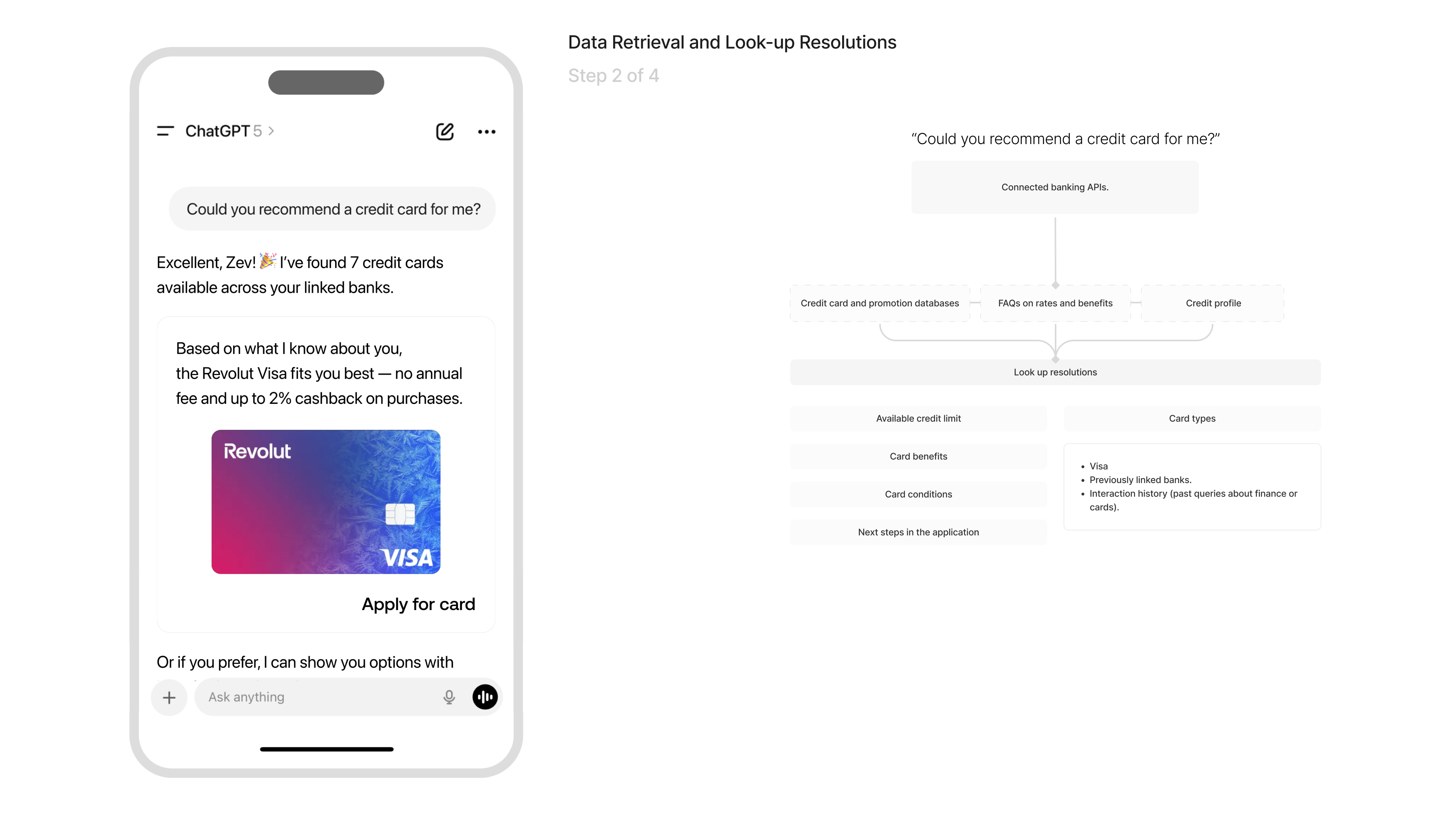

Data Retrieval and Look-up Resolutions

Purpose: Retrieve real banking data and surface actionable recommendations.

ChatGPT connects to banking APIs to retrieve real financial information such as available credit limits, active promotions, card conditions, and the user’s credit profile and uses this data to generate a tailored recommendation.

The assistant combines live banking information with the user’s context and interaction history to surface the most relevant credit-card option, presenting it in a natural, human-like way. This step demonstrates the system’s ability to merge backend data with conversational intelligence, creating a recommendation flow that feels highly personalized, accurate, and immediately actionable.

Demonstrates real-time financial recommendation capability, blending live banking data with contextual knowledge.

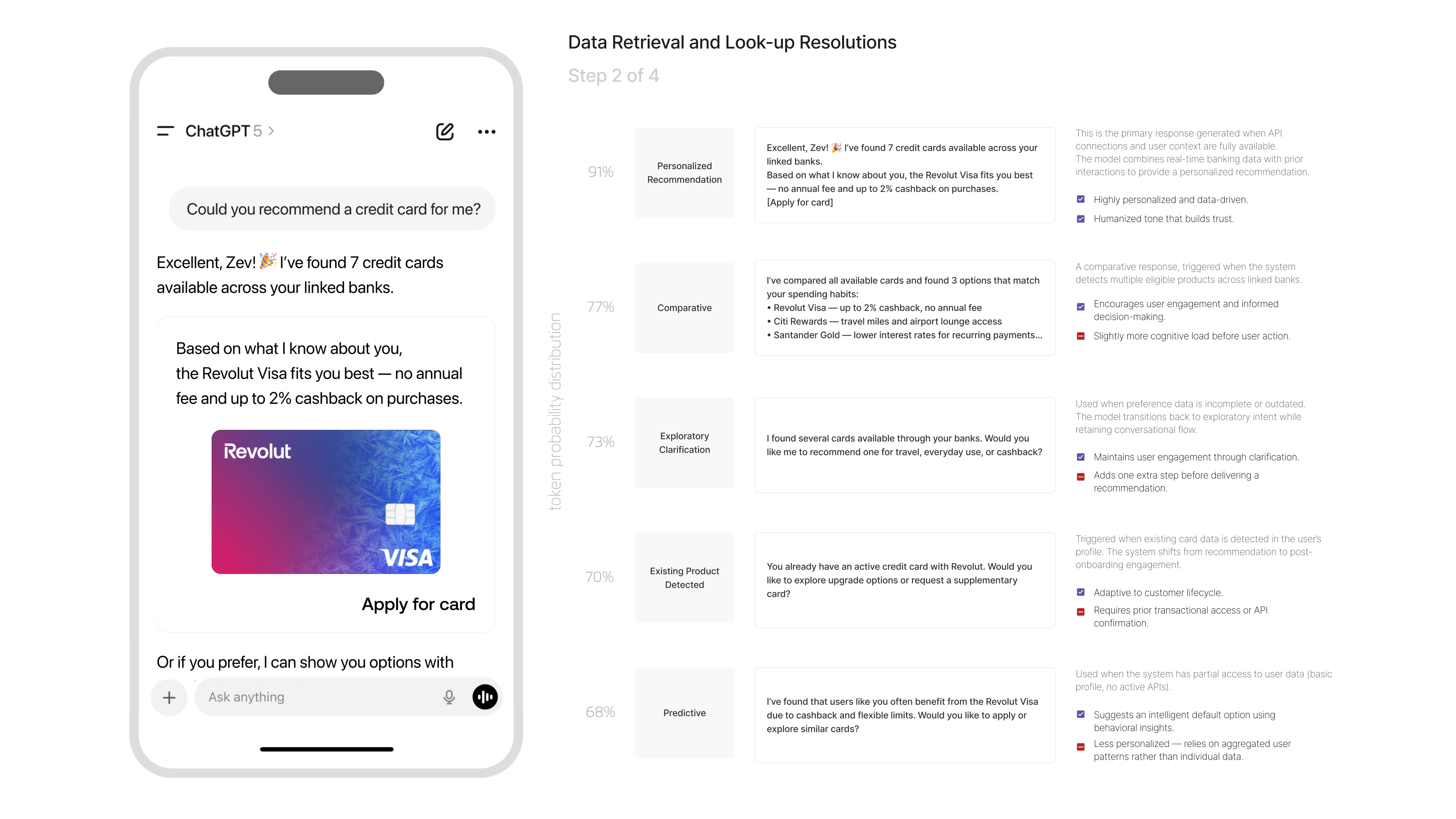

The system determines how it should present card recommendations by comparing different reasoning patterns ranging from highly personalized suggestions to broader comparative analysis or exploratory clarification based on the data retrieved through banking APIs.

It evaluates which path will deliver the most relevant, trustworthy, and helpful answer depending on the completeness and freshness of the user’s data. By understanding whether the user already has a card, whether their preferences are known, or whether predictive modelling might be helpful, the model selects the most appropriate conversation style.

This adaptive decision-making creates a fluid, context-aware recommendation experience that feels personal and intelligent rather than generic.

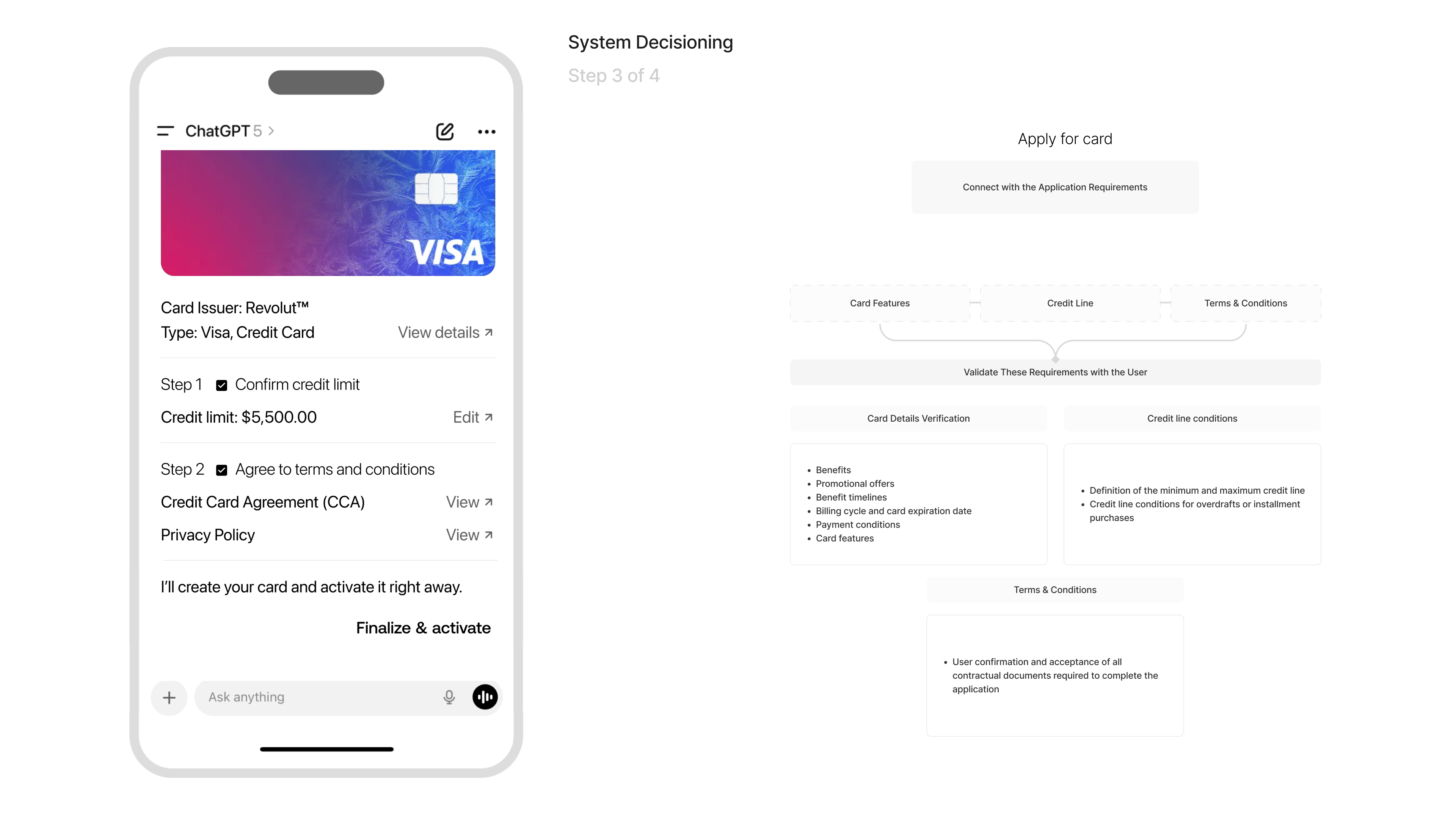

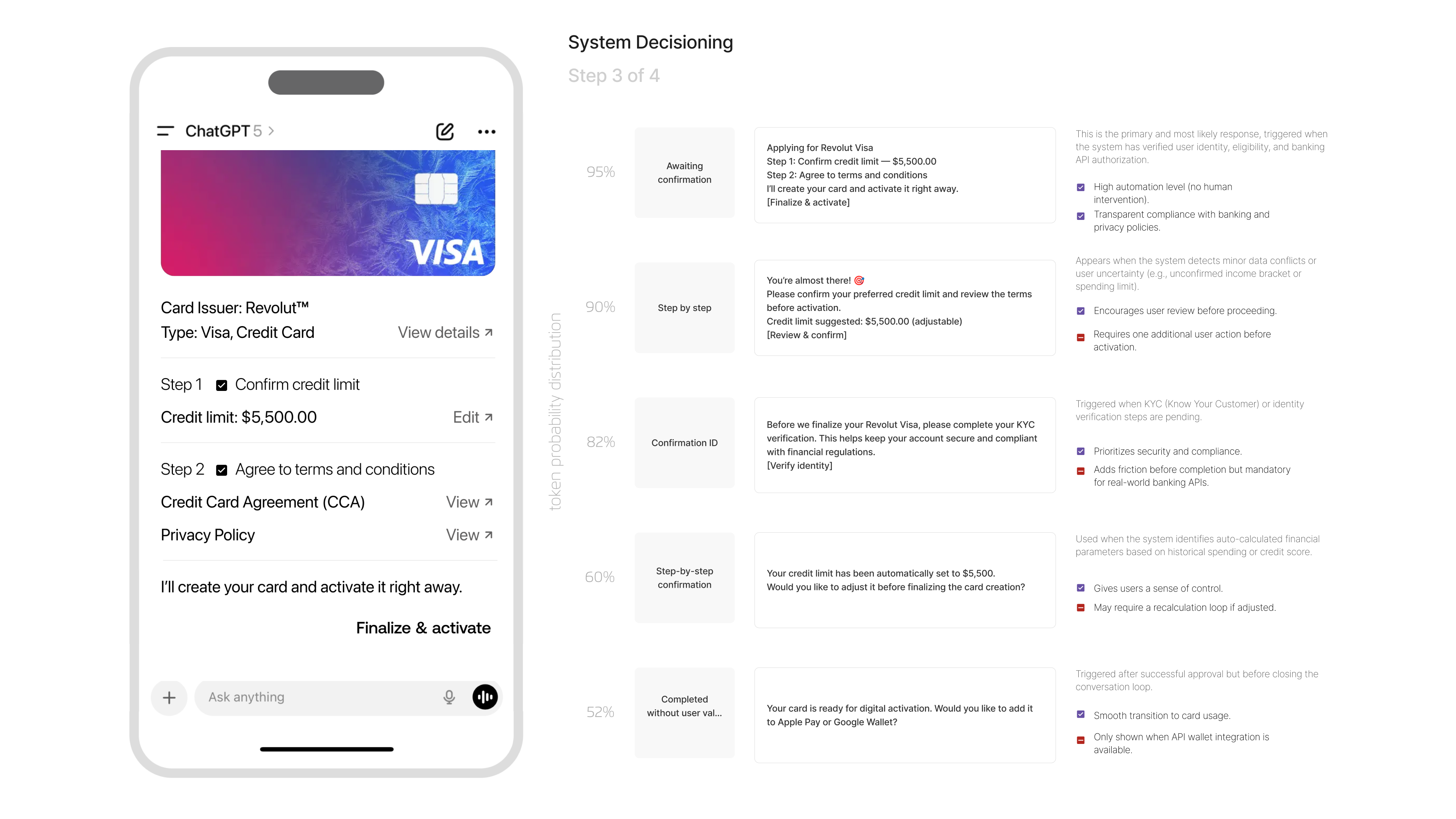

System Decisioning

Purpose: Formalize the credit decision and guide the user through activation.

Step 3 focuses on the approval and creation of the credit card, where ChatGPT validates key requirements such as credit limits, eligibility, promotional benefits, and regulatory disclosures. The assistant guides the user through confirming the credit line and agreeing to the terms and conditions, while internally ensuring full compliance with credit-decision rules and KYC policies. This phase reflects how the system can automate complex financial decisioning behind the scenes while keeping the user experience simple, transparent, and friction-controlled.

Simulates a real credit-decision process, combining automation with transparency and regulatory compliance.

The extended decisioning shows how the system navigates between different approval pathways depending on the user’s eligibility, identity verification status, and data confidence levels.

The model chooses between immediate confirmation, a step-by-step review, additional KYC validation, auto-calculated credit-limit confirmation, or even completing the process without user intervention if sufficient data is already verified.

Each path reflects a different level of friction, safety, and autonomy, allowing the system to adapt to real-world banking rules while still keeping the experience smooth. This ensures the approval flow remains compliant, secure, and personalized, adjusting dynamically to what the system knows or still needs to validate.

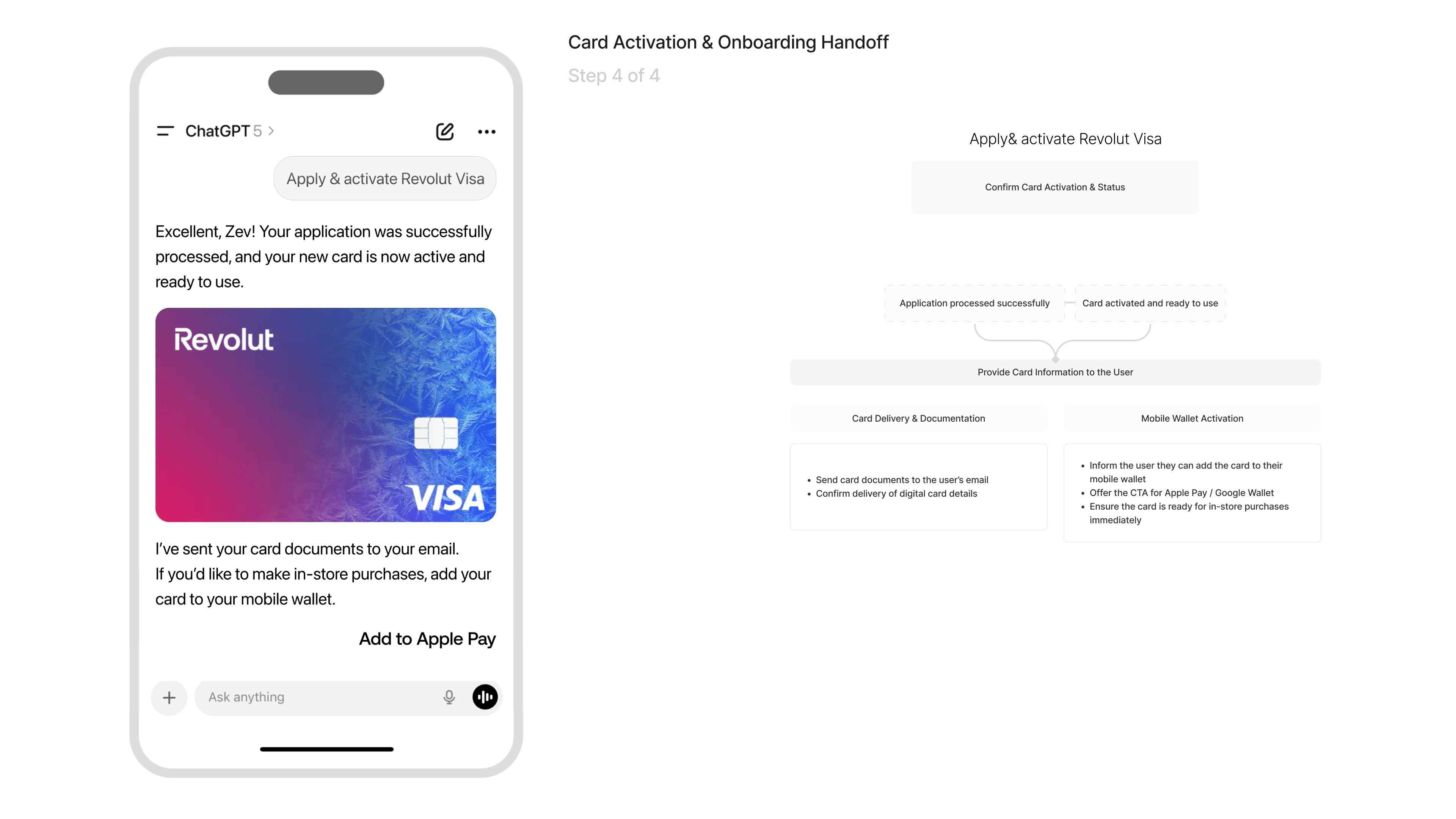

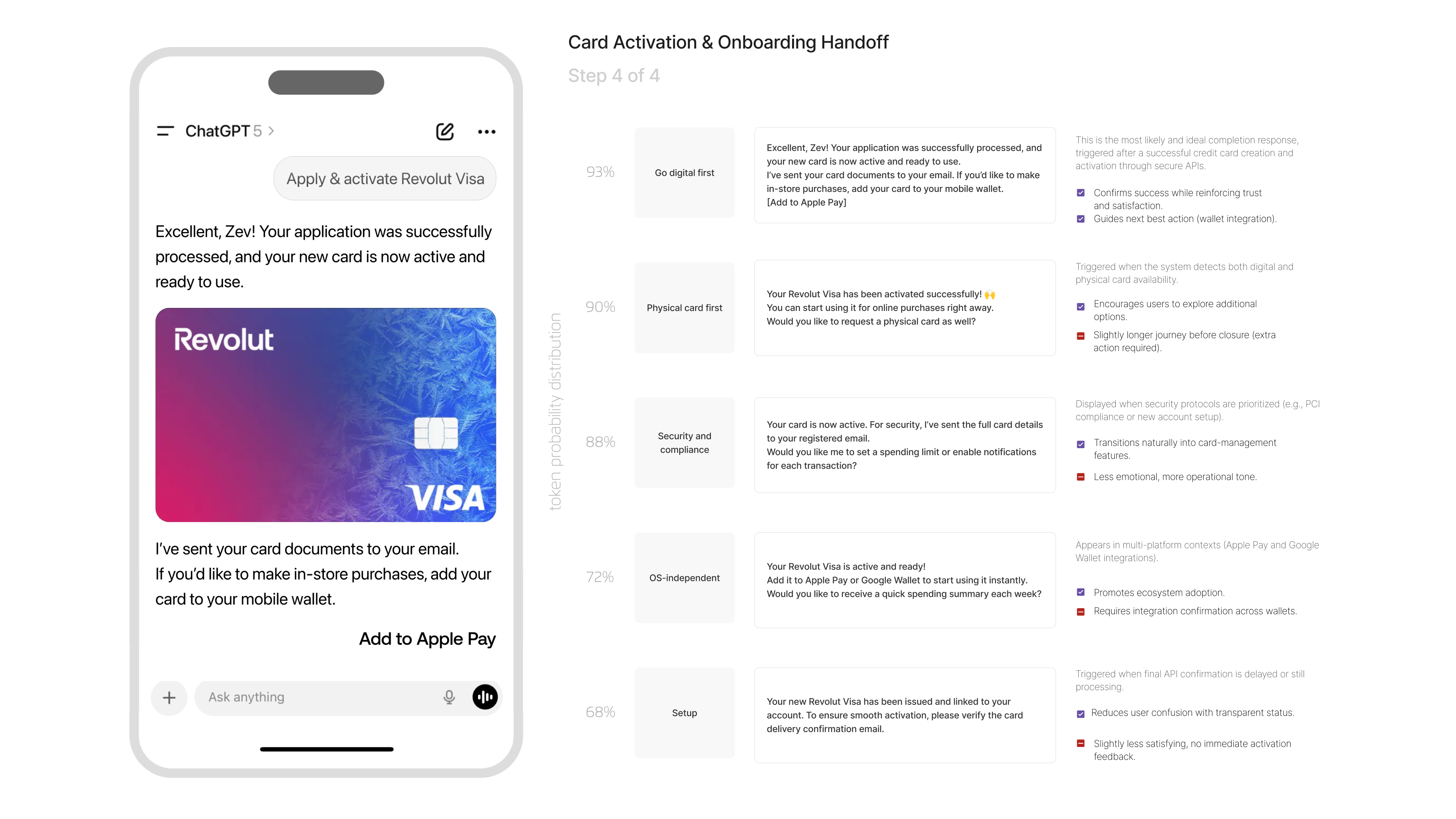

Card Activation & Onboarding Handoff

Purpose: Confirm activation and complete digital onboarding.

In the final step completes the process by activating the newly issued card and delivering all relevant digital documents to the user. The system then guides the user into immediate usage through mobile-wallet onboarding, offering a seamless call-to-action to add the card to Apple Pay or Google Wallet. This step closes the end-to-end journey by transitioning smoothly from approval to real-world usability, ensuring the user can start making purchases instantly through the same conversational interface.

Completes the end-to-end credit-card journey, from intent to activation, in a single conversational interface.

Now the system evaluates several possible closing states for the onboarding flow, choosing the one that best matches the user’s context, device, and activation status.

Based on the final API confirmation, it may emphasize digital activation with Apple Pay, offer the option to request a physical card, transition into a security-focused message, or provide an OS-independent handoff compatible with both Apple and Google wallets.

The system dynamically selects the closing message that reinforces trust, clarity, and next steps, ensuring the user knows exactly how to start using their new card immediately. This creates a seamless and intelligent wrap-up to the entire credit-card journey.

Using banking APIs ChatGPT can securely connect and analyze your financial data.

Explore the prototype

Learnings & Reflections

This project helped me recognize how limited traditional design approaches are when dealing with highly fragmented financial journeys. The real complexity wasn’t in redesigning screens it was in orchestrating intelligent decision-making, connecting banking APIs with a conversational AI, and demonstrating that strategic design can also shape reasoning models, regulatory compliance, and real credit-decision flows.

I learned that AI’s true differentiation isn’t in generating answers, but in reasoning through multiple decision paths based on user profiles, data freshness, and risk levels. Integrating banking APIs with ChatGPT requires a radically different mindset closer to defining security policies, intent models, and validation routes than to designing interfaces. In complex products, design must act as a bridge between business, technology, risk, and user experience, articulating not only what is shown, but how an AI decides.

Conversational flows can replace entire user journeys, but only when modeled responsibly, ensuring compliance, accuracy, limitations, disclosures, KYC, and experience coexist without friction.

This project reinforced my belief that the future of digital banking design won’t be visual-first—it will be reasoning-first.

What I’m Most Proud Of

I’m particularly proud of taking this project far beyond a visual prototype and building a complete simulation of how a financial AI assistant should think classifying intent, selecting secure resolution paths, balancing compliance with personalization, and guiding an end-to-end credit-card journey from recommendation to activation.

It demonstrates how a single conversation can evolve into an intelligent, secure, and fully actionable financial experience.

What I Would Have Done Differently

If I were to do this again, I would go deeper into bank-specific rules, incorporate error and failure scenarios to strengthen system resilience, and design conversation-based decision paths that adapt to user history. These enhancements would have added even greater regulatory realism and produced a more adaptive behavior aligned with a production-ready system.

What I Would Do Next

The next step would be to evolve this concept into a real financial-orchestration platform integrating regulated open-banking APIs, a more robust credit-decision engine, transparent multi-criteria comparisons, simulation tools for bank teams, and extending the model into other financial products such as loans, insurance, and investments, creating a fully connected, AI-driven conversational ecosystem.

2025

Connecting banking apps with ChatGPT to redefine how users choose credit cards.

José Manuel Zevallos, Stanford University

Rol

Product Design

UX Strategy

UI Design

Category

FintechAI IntegrationiOS / Android

Project Type

BankingConversational AIConcept Design

Challenge

Today, users must manually compare multiple banking apps to understand which credit card best fits their needs. Each bank promotes its own products, creating fragmented, biased, and time-consuming experiences. This complexity not only limits transparency but also increases friction in decision-making, leaving users overwhelmed and often choosing suboptimal cards. There is no unified experience that helps users make smart, personalized financial decisions across institutions.

Hypothesis

If banking apps were securely connected through ChatGPT, users could authenticate once and instantly compare their eligibility, benefits, and offers across all their banks. By combining conversational AI with secure login (Face ID + API integrations), users would receive objective recommendations based on preferences, such as cashback, travel, or dining rewards reducing friction, improving trust, and accelerating credit-card adoption.

Summary

This proof of concept explores how ChatGPT can serve as a financial orchestrator, connecting multiple banking apps to redefine how users choose and request credit cards. By unifying authentication and decision-making into a single conversational experience, the flow empowers users with clarity, personalization, and control, while helping banks increase product visibility and digital conversion.

Problem Users Faced

Users struggle to identify which credit card offers the best value without logging into multiple apps, reading complex terms, or comparing unclear benefits. The current process is tedious, opaque, and biased toward each bank’s ecosystem, discouraging users from exploring better options.

Business Objective

To enable a cross-banking, AI-driven experience that increases user engagement and conversion rates for credit-card products, while positioning the bank ecosystem as transparent, data-driven, and customer-centric through open-banking integrations with ChatGPT.

Product Owner & Business Request

The Product Owner requested a conceptual prototype demonstrating how an AI assistant like ChatGPT could integrate securely with multiple banking apps to streamline credit-card discovery and acquisition. The goal is to validate the potential impact on user trust, conversion rate, and perceived innovation through a seamless conversational flow.

Applied Methodology

This project applies a Lean Product Discovery & AI-Driven Design methodology, combining Service Design, Human-Centered Design (HCD), and Experiment-Based Validation to explore how conversational interfaces can transform cross-banking experiences.

Proof of concept (PoC) English

Proof of concept (PoC) Spanish

Recognition of Request

Purpose: Understand the user’s intent and classify the type of request.

At this stage, the system interprets the message “Could you recommend a credit card for me?”.ChatGPT identifies the user’s goal (getting a credit card recommendation) and determines whether the request is informational or action-oriented.It then performs a structured lookup across different resolution paths:

- Intent classification: Determines whether the user wants a general list of cards or a personalized recommendation based on their profile.

- Entity recognition: Detects keywords like “credit card” and pronouns like “for me”, which signal personalization.

- Context processing & retrieval: Considers location, linked banks, and interaction history.

This step ensures contextual accuracy, compliance, and personalization before the model proceeds.

The system evaluates multiple possible response styles based on the user’s request, weighing each option according to regulatory constraints, personalization requirements, and conversational context.

It analyzes whether the best response is a secure API-connection prompt, a more exploratory conversational reply, a simulated example, a clarifying question, or a predictive suggestion.

The model does this by calculating token-level probability distributions for each reasoning path, ultimately selecting the approach that balances compliance, personalization, and user intent. This ensures that before any action is taken, the assistant understands both what the user wants and the safest, most accurate way to proceed.

Data Retrieval and Look-up Resolutions

Purpose: Retrieve real banking data and surface actionable recommendations.

ChatGPT connects to banking APIs to retrieve real financial information such as available credit limits, active promotions, card conditions, and the user’s credit profile and uses this data to generate a tailored recommendation.

The assistant combines live banking information with the user’s context and interaction history to surface the most relevant credit-card option, presenting it in a natural, human-like way. This step demonstrates the system’s ability to merge backend data with conversational intelligence, creating a recommendation flow that feels highly personalized, accurate, and immediately actionable.

Demonstrates real-time financial recommendation capability, blending live banking data with contextual knowledge.

The system determines how it should present card recommendations by comparing different reasoning patterns ranging from highly personalized suggestions to broader comparative analysis or exploratory clarification based on the data retrieved through banking APIs.

It evaluates which path will deliver the most relevant, trustworthy, and helpful answer depending on the completeness and freshness of the user’s data. By understanding whether the user already has a card, whether their preferences are known, or whether predictive modelling might be helpful, the model selects the most appropriate conversation style.

This adaptive decision-making creates a fluid, context-aware recommendation experience that feels personal and intelligent rather than generic.

System Decisioning

Purpose: Formalize the credit decision and guide the user through activation.

Step 3 focuses on the approval and creation of the credit card, where ChatGPT validates key requirements such as credit limits, eligibility, promotional benefits, and regulatory disclosures. The assistant guides the user through confirming the credit line and agreeing to the terms and conditions, while internally ensuring full compliance with credit-decision rules and KYC policies. This phase reflects how the system can automate complex financial decisioning behind the scenes while keeping the user experience simple, transparent, and friction-controlled.

Simulates a real credit-decision process, combining automation with transparency and regulatory compliance.

The extended decisioning shows how the system navigates between different approval pathways depending on the user’s eligibility, identity verification status, and data confidence levels.

The model chooses between immediate confirmation, a step-by-step review, additional KYC validation, auto-calculated credit-limit confirmation, or even completing the process without user intervention if sufficient data is already verified.

Each path reflects a different level of friction, safety, and autonomy, allowing the system to adapt to real-world banking rules while still keeping the experience smooth. This ensures the approval flow remains compliant, secure, and personalized, adjusting dynamically to what the system knows or still needs to validate.

Card Activation & Onboarding Handoff

Purpose: Confirm activation and complete digital onboarding.

In the final step completes the process by activating the newly issued card and delivering all relevant digital documents to the user. The system then guides the user into immediate usage through mobile-wallet onboarding, offering a seamless call-to-action to add the card to Apple Pay or Google Wallet. This step closes the end-to-end journey by transitioning smoothly from approval to real-world usability, ensuring the user can start making purchases instantly through the same conversational interface.

Completes the end-to-end credit-card journey, from intent to activation, in a single conversational interface.

Now the system evaluates several possible closing states for the onboarding flow, choosing the one that best matches the user’s context, device, and activation status.

Based on the final API confirmation, it may emphasize digital activation with Apple Pay, offer the option to request a physical card, transition into a security-focused message, or provide an OS-independent handoff compatible with both Apple and Google wallets.

The system dynamically selects the closing message that reinforces trust, clarity, and next steps, ensuring the user knows exactly how to start using their new card immediately. This creates a seamless and intelligent wrap-up to the entire credit-card journey.

Using banking APIs ChatGPT can securely connect and analyze your financial data.

Explore the prototype

Learnings & Reflections

This project helped me recognize how limited traditional design approaches are when dealing with highly fragmented financial journeys. The real complexity wasn’t in redesigning screens it was in orchestrating intelligent decision-making, connecting banking APIs with a conversational AI, and demonstrating that strategic design can also shape reasoning models, regulatory compliance, and real credit-decision flows.

I learned that AI’s true differentiation isn’t in generating answers, but in reasoning through multiple decision paths based on user profiles, data freshness, and risk levels. Integrating banking APIs with ChatGPT requires a radically different mindset closer to defining security policies, intent models, and validation routes than to designing interfaces. In complex products, design must act as a bridge between business, technology, risk, and user experience, articulating not only what is shown, but how an AI decides.

Conversational flows can replace entire user journeys, but only when modeled responsibly, ensuring compliance, accuracy, limitations, disclosures, KYC, and experience coexist without friction.

This project reinforced my belief that the future of digital banking design won’t be visual-first—it will be reasoning-first.

What I’m Most Proud Of

I’m particularly proud of taking this project far beyond a visual prototype and building a complete simulation of how a financial AI assistant should think classifying intent, selecting secure resolution paths, balancing compliance with personalization, and guiding an end-to-end credit-card journey from recommendation to activation.

It demonstrates how a single conversation can evolve into an intelligent, secure, and fully actionable financial experience.

What I Would Have Done Differently

If I were to do this again, I would go deeper into bank-specific rules, incorporate error and failure scenarios to strengthen system resilience, and design conversation-based decision paths that adapt to user history. These enhancements would have added even greater regulatory realism and produced a more adaptive behavior aligned with a production-ready system.

What I Would Do Next

The next step would be to evolve this concept into a real financial-orchestration platform integrating regulated open-banking APIs, a more robust credit-decision engine, transparent multi-criteria comparisons, simulation tools for bank teams, and extending the model into other financial products such as loans, insurance, and investments, creating a fully connected, AI-driven conversational ecosystem.

Professional website of José Manuel Zevallos

Digital Media Designer © 2025. All rights reserved.

zevallosj147@gmail.com

LinkedIn: in/jmanuelzevallos

2025

Connecting banking apps with ChatGPT to redefine how users choose credit cards.

José Manuel Zevallos, Stanford University

Challenge

Today, users must manually compare multiple banking apps to understand which credit card best fits their needs. Each bank promotes its own products, creating fragmented, biased, and time-consuming experiences. This complexity not only limits transparency but also increases friction in decision-making, leaving users overwhelmed and often choosing suboptimal cards. There is no unified experience that helps users make smart, personalized financial decisions across institutions.

Hypothesis

If banking apps were securely connected through ChatGPT, users could authenticate once and instantly compare their eligibility, benefits, and offers across all their banks. By combining conversational AI with secure login (Face ID + API integrations), users would receive objective recommendations based on preferences, such as cashback, travel, or dining rewards reducing friction, improving trust, and accelerating credit-card adoption.

Summary

This proof of concept explores how ChatGPT can serve as a financial orchestrator, connecting multiple banking apps to redefine how users choose and request credit cards. By unifying authentication and decision-making into a single conversational experience, the flow empowers users with clarity, personalization, and control, while helping banks increase product visibility and digital conversion.

Problem Users Faced

Users struggle to identify which credit card offers the best value without logging into multiple apps, reading complex terms, or comparing unclear benefits. The current process is tedious, opaque, and biased toward each bank’s ecosystem, discouraging users from exploring better options.

Business Objective

To enable a cross-banking, AI-driven experience that increases user engagement and conversion rates for credit-card products, while positioning the bank ecosystem as transparent, data-driven, and customer-centric through open-banking integrations with ChatGPT.

Product Owner & Business Request

The Product Owner requested a conceptual prototype demonstrating how an AI assistant like ChatGPT could integrate securely with multiple banking apps to streamline credit-card discovery and acquisition. The goal is to validate the potential impact on user trust, conversion rate, and perceived innovation through a seamless conversational flow.

Applied Methodology

This project applies a Lean Product Discovery & AI-Driven Design methodology, combining Service Design, Human-Centered Design (HCD), and Experiment-Based Validation to explore how conversational interfaces can transform cross-banking experiences.

Proof of concept (PoC) English

Proof of concept (PoC) Spanish

Recognition of Request

Purpose: Understand the user’s intent and classify the type of request.

At this stage, the system interprets the message “Could you recommend a credit card for me?”.ChatGPT identifies the user’s goal (getting a credit card recommendation) and determines whether the request is informational or action-oriented.It then performs a structured lookup across different resolution paths:

- Intent classification: Determines whether the user wants a general list of cards or a personalized recommendation based on their profile.

- Entity recognition: Detects keywords like “credit card” and pronouns like “for me”, which signal personalization.

- Context processing & retrieval: Considers location, linked banks, and interaction history.

This step ensures contextual accuracy, compliance, and personalization before the model proceeds.

The system evaluates multiple possible response styles based on the user’s request, weighing each option according to regulatory constraints, personalization requirements, and conversational context.

It analyzes whether the best response is a secure API-connection prompt, a more exploratory conversational reply, a simulated example, a clarifying question, or a predictive suggestion.

The model does this by calculating token-level probability distributions for each reasoning path, ultimately selecting the approach that balances compliance, personalization, and user intent. This ensures that before any action is taken, the assistant understands both what the user wants and the safest, most accurate way to proceed.

Data Retrieval and Look-up Resolutions

Purpose: Retrieve real banking data and surface actionable recommendations.

ChatGPT connects to banking APIs to retrieve real financial information such as available credit limits, active promotions, card conditions, and the user’s credit profile and uses this data to generate a tailored recommendation.

The assistant combines live banking information with the user’s context and interaction history to surface the most relevant credit-card option, presenting it in a natural, human-like way. This step demonstrates the system’s ability to merge backend data with conversational intelligence, creating a recommendation flow that feels highly personalized, accurate, and immediately actionable.

Demonstrates real-time financial recommendation capability, blending live banking data with contextual knowledge.

The system determines how it should present card recommendations by comparing different reasoning patterns ranging from highly personalized suggestions to broader comparative analysis or exploratory clarification based on the data retrieved through banking APIs.

It evaluates which path will deliver the most relevant, trustworthy, and helpful answer depending on the completeness and freshness of the user’s data. By understanding whether the user already has a card, whether their preferences are known, or whether predictive modelling might be helpful, the model selects the most appropriate conversation style.

This adaptive decision-making creates a fluid, context-aware recommendation experience that feels personal and intelligent rather than generic.

System Decisioning

Purpose: Formalize the credit decision and guide the user through activation.

Step 3 focuses on the approval and creation of the credit card, where ChatGPT validates key requirements such as credit limits, eligibility, promotional benefits, and regulatory disclosures. The assistant guides the user through confirming the credit line and agreeing to the terms and conditions, while internally ensuring full compliance with credit-decision rules and KYC policies. This phase reflects how the system can automate complex financial decisioning behind the scenes while keeping the user experience simple, transparent, and friction-controlled.

Simulates a real credit-decision process, combining automation with transparency and regulatory compliance.

The extended decisioning shows how the system navigates between different approval pathways depending on the user’s eligibility, identity verification status, and data confidence levels.

The model chooses between immediate confirmation, a step-by-step review, additional KYC validation, auto-calculated credit-limit confirmation, or even completing the process without user intervention if sufficient data is already verified.

Each path reflects a different level of friction, safety, and autonomy, allowing the system to adapt to real-world banking rules while still keeping the experience smooth. This ensures the approval flow remains compliant, secure, and personalized, adjusting dynamically to what the system knows or still needs to validate.

Card Activation & Onboarding Handoff

Purpose: Confirm activation and complete digital onboarding.

In the final step completes the process by activating the newly issued card and delivering all relevant digital documents to the user. The system then guides the user into immediate usage through mobile-wallet onboarding, offering a seamless call-to-action to add the card to Apple Pay or Google Wallet. This step closes the end-to-end journey by transitioning smoothly from approval to real-world usability, ensuring the user can start making purchases instantly through the same conversational interface.

Completes the end-to-end credit-card journey, from intent to activation, in a single conversational interface.

Now the system evaluates several possible closing states for the onboarding flow, choosing the one that best matches the user’s context, device, and activation status.

Based on the final API confirmation, it may emphasize digital activation with Apple Pay, offer the option to request a physical card, transition into a security-focused message, or provide an OS-independent handoff compatible with both Apple and Google wallets.

The system dynamically selects the closing message that reinforces trust, clarity, and next steps, ensuring the user knows exactly how to start using their new card immediately. This creates a seamless and intelligent wrap-up to the entire credit-card journey.

Using banking APIs ChatGPT can securely connect and analyze your financial data.

Explore the prototype

Learnings & Reflections

This project helped me recognize how limited traditional design approaches are when dealing with highly fragmented financial journeys. The real complexity wasn’t in redesigning screens it was in orchestrating intelligent decision-making, connecting banking APIs with a conversational AI, and demonstrating that strategic design can also shape reasoning models, regulatory compliance, and real credit-decision flows.

I learned that AI’s true differentiation isn’t in generating answers, but in reasoning through multiple decision paths based on user profiles, data freshness, and risk levels. Integrating banking APIs with ChatGPT requires a radically different mindset closer to defining security policies, intent models, and validation routes than to designing interfaces. In complex products, design must act as a bridge between business, technology, risk, and user experience, articulating not only what is shown, but how an AI decides.

Conversational flows can replace entire user journeys, but only when modeled responsibly, ensuring compliance, accuracy, limitations, disclosures, KYC, and experience coexist without friction.

This project reinforced my belief that the future of digital banking design won’t be visual-first—it will be reasoning-first.

What I’m Most Proud Of

I’m particularly proud of taking this project far beyond a visual prototype and building a complete simulation of how a financial AI assistant should think classifying intent, selecting secure resolution paths, balancing compliance with personalization, and guiding an end-to-end credit-card journey from recommendation to activation.

It demonstrates how a single conversation can evolve into an intelligent, secure, and fully actionable financial experience.

What I Would Have Done Differently

If I were to do this again, I would go deeper into bank-specific rules, incorporate error and failure scenarios to strengthen system resilience, and design conversation-based decision paths that adapt to user history. These enhancements would have added even greater regulatory realism and produced a more adaptive behavior aligned with a production-ready system.

What I Would Do Next

The next step would be to evolve this concept into a real financial-orchestration platform integrating regulated open-banking APIs, a more robust credit-decision engine, transparent multi-criteria comparisons, simulation tools for bank teams, and extending the model into other financial products such as loans, insurance, and investments, creating a fully connected, AI-driven conversational ecosystem.

Rol

Product Design

UX Strategy

UI Design

Category

FintechAI IntegrationiOS / Android

Project Type

BankingConversational AIConcept Design

Professional website of José Manuel Zevallos

Digital Media Designer © 2025. All rights reserved.

zevallosj147@gmail.com

LinkedIn: in/jmanuelzevallos